America’s industrial economy is starting to look different than it did even a few years ago.

For decades, the dominant assumption across manufacturing and supply chains was that efficiency would always outweigh resilience. Companies optimized for lower costs, longer supply chains, and concentrated production capacity overseas because the system appeared stable enough to support it. But the last several years — from COVID disruptions to geopolitical instability to growing defense demands — have exposed just how fragile that model really was.

This week’s manufacturing headlines reinforced something that is becoming increasingly difficult to ignore: capacity matters again.

U.S. factory output posted its strongest monthly gain in more than a year, driven by automotive production, semiconductors, and communications equipment. At the same time, billions of dollars flowed into defense manufacturing, energy infrastructure, missile production, drones, and advanced industrial technologies. The common thread across nearly all of it is strategic capacity building — not simply expanding production for the sake of growth, but rebuilding the ability to produce critical systems domestically when it matters most.

And increasingly, defense spending is becoming one of the primary accelerants behind that shift.

For years, conversations around the defense industrial base focused mostly on procurement budgets and weapons platforms. Now the discussion is moving deeper into the underlying manufacturing ecosystem itself: supplier networks, rocket motors, batteries, semiconductors, production tooling, workforce constraints, and surge capacity. That’s a meaningful change because manufacturing strength has never been just about the largest contractors. It’s about the long tail of small and mid-sized manufacturers that actually make the industrial system resilient.

The challenge is that rebuilding distributed manufacturing capacity after decades of consolidation is not simple or fast. Some sectors are scaling aggressively while others are still restructuring around old globalization-era assumptions. That tension showed up repeatedly this week as major industrial investments expanded alongside continued layoffs and operational restructuring activity across legacy manufacturers.

Still, the broader direction is becoming clearer. The United States is entering the early stages of a long-term industrial realignment centered around domestic capacity, strategic resilience, and rebuilding manufacturing ecosystems that can support both economic competitiveness and national security.

Defense Manufacturing Is Becoming America’s Industrial Growth Engine

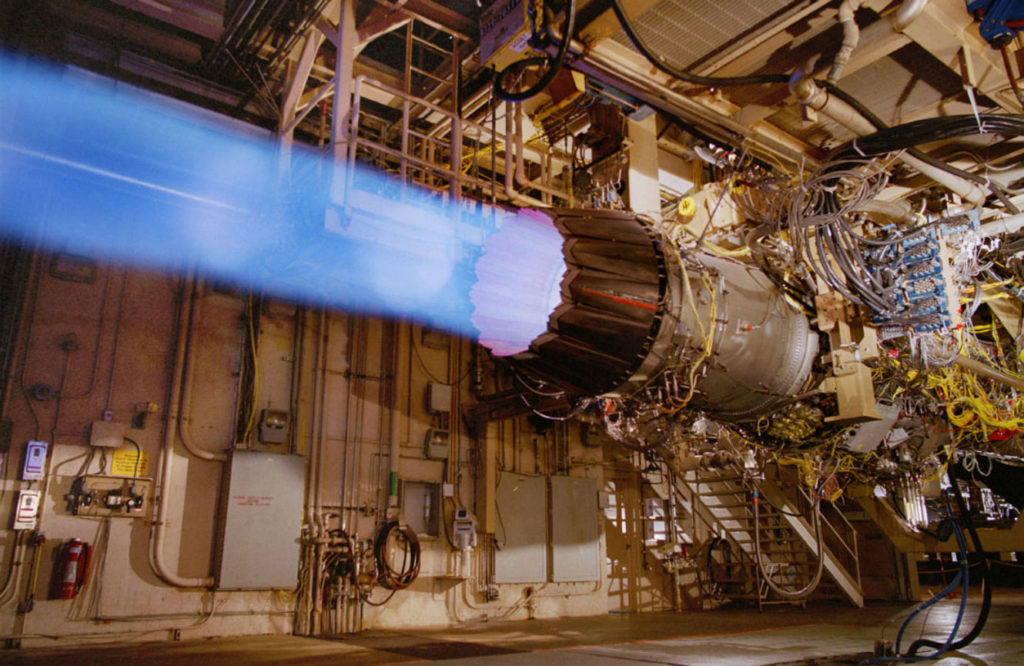

One of the clearest stories this week was the scale of investment now flowing into defense manufacturing capacity.

Anduril Industries announced a massive $5 billion funding round that will be used to expand manufacturing infrastructure, research and development, and production capabilities tied to defense systems. Alongside that announcement, Anduril and several partner firms signed agreements tied to supplying the Department of Defense with 10,000 missiles over the next several years.

Meanwhile, the Pentagon announced another $191 million in investments into the domestic solid rocket motor industrial base under Defense Production Act authorities. Additional framework agreements with Lockheed Martin, Honeywell, and BAE Systems are also intended to accelerate missile and precision weapons production while rebuilding depleted stockpiles.

The important point here is that these announcements are not isolated procurement decisions. They reflect a larger realization inside both government and industry that industrial depth itself is now a strategic asset.

For decades, efficiency-driven consolidation reduced redundancy across the defense industrial base. Production became increasingly concentrated among fewer suppliers, longer lead times became normalized, and surge manufacturing capability steadily eroded. That system works reasonably well during stable periods. It works far less effectively when geopolitical instability rises or when conflicts consume munitions faster than production lines can replenish them.

What appears to be happening now is a deliberate effort to rebuild optionality into the system.

That includes expanding domestic missile production, reshoring battery and drone supply chains to comply with NDAA sourcing requirements, and broadening the supplier ecosystem supporting defense manufacturing. Companies like EagleNXT launching domestic drone manufacturing facilities may seem small in isolation, but collectively these distributed investments matter because resilience comes from networks, not single factories.

This is particularly important for small and medium-sized manufacturers. The defense industrial base cannot scale effectively if participation is limited to a handful of giant contractors. Real industrial resilience comes from thousands of specialized manufacturers working together across regions, capabilities, and production tiers.

In many ways, the Pentagon is rediscovering something manufacturers have always understood: manufacturing is a team sport done in community.

AI Is Quietly Becoming A Manufacturing Story

Artificial intelligence continues to dominate technology conversations, but one of the most underappreciated developments right now is how quickly AI demand is translating into physical industrial expansion.

The strongest contributors to this month’s factory output growth were semiconductors, communications equipment, and other high-tech manufacturing sectors tied directly to AI infrastructure growth. But the effects are spreading much further than chip production itself.

This week, TS Conductor opened a new $134 million manufacturing facility in South Carolina focused on advanced conductors designed to increase electrical grid capacity. The reason? Rising electricity demand associated with AI data centers and high-density computing infrastructure.

That’s an important signal.

Every major technological shift eventually becomes a manufacturing story because digital systems still require physical infrastructure: semiconductors, transformers, cooling systems, power equipment, communications hardware, and industrial materials. AI may appear software-driven on the surface, but underneath it sits an enormous industrial footprint.

The semiconductor ecosystem itself also continues deepening domestically. Lam Research expanded its Idaho presence to support collaborative R&D and manufacturing activity tied to Micron and broader U.S. semiconductor growth initiatives.

Taken together, these developments suggest that AI is becoming a force multiplier for domestic industrial investment. And unlike previous technology cycles that heavily concentrated wealth in software platforms, this one has the potential to create broader downstream manufacturing demand across energy systems, industrial equipment, advanced materials, and infrastructure manufacturing.

That matters because manufacturing ecosystems thrive when demand ripples outward across supplier networks.

Reshoring Continues — But The Transition Remains Uneven

While new investments continue accelerating, this week also highlighted the reality that industrial transitions are rarely smooth.

Discussions surrounding layoffs at General Motors and reports tied to the Goodyear plant closure in Fayetteville reflect the difficult restructuring that continues across portions of the industrial economy. Some companies are investing aggressively into future domestic capacity while others are still navigating the financial and operational consequences of globalization-era manufacturing models.

That tension is likely to continue for years.

Reshoring is not simply about announcing new factories. It requires rebuilding supplier relationships, workforce pipelines, tooling expertise, and production ecosystems that were hollowed out over multiple decades. In many sectors, domestic manufacturing capacity cannot simply be turned back on overnight because the supporting industrial networks no longer fully exist.

At the same time, global competitive pressures are intensifying rather than easing. India continues accelerating its own semiconductor ambitions through partnerships like the new Tata-ASML agreement, while AUKUS submarine production challenges exposed ongoing bottlenecks inside America’s naval industrial base.

The broader point is that the industrial realignment now underway is happening inside a highly competitive and increasingly fragmented global environment. Every country is trying to secure strategic manufacturing capacity at the same time.

The encouraging part is that the United States still possesses enormous distributed manufacturing capability across its network of small and medium-sized businesses. The challenge has never been a lack of talent or industrial expertise. More often, it’s been visibility, coordination, and investment.

That’s why this current moment matters so much.

We are still likely in the first or second inning of a twenty-to-thirty-year secular shift toward localized manufacturing supply chains and greater industrial resilience. The companies that invest now — in relationships, domestic supplier networks, workforce capability, and production infrastructure — will be positioned to lead the next era of American manufacturing.

And increasingly, the market is beginning to reward exactly that.