June 2026 Manufacturing Insights

U.S. manufacturing kept growing in June 2026, but the ground shifted beneath the headline numbers. Both major purchasing manager surveys stayed comfortably in expansion territory, yet the same reports show factories cutting jobs at the fastest pace in years, even as order books fill up.

Input costs finally eased, with the ISM Prices Index posting its largest one-month drop in nearly four years as Middle East tensions cooled. Capital investment told a confident story too. June delivered JetZero’s $4.7 billion aerospace campus in North Carolina and a $1.2 billion rare earth magnet plant in South Carolina aimed squarely at China’s grip on critical minerals.

A Month in Manufacturing Data

Perspectives from the ISM Report

The ISM Manufacturing PMI registered 53.3 percent in June, down 0.7 percentage point from May’s 54.0 percent but marking a sixth consecutive month of expansion, the sector’s longest streak since 2022. ISM notes the reading corresponds to roughly 2 percent annualized GDP growth, and 14 of 18 industries reported growth.

Demand stayed solid. The New Orders Index came in at 56 percent, down slightly from May’s 56.8 percent, while production grew at a slower 52.2 percent. Four of the six largest manufacturing industries reported higher new orders, led by Computer and Electronic Products and Machinery.

The biggest story was prices. The Prices Index fell 9.1 percentage points to 73 percent, the largest single-month decline since July 2022, though 15 of 18 industries still reported paying more for inputs. Employment improved to 49.7 percent, still contracting but the strongest reading since January 2025, and 64 percent of panelists said their companies are hiring, nearly reversing January’s numbers. Inventories returned to expansion for the first time in 13 months, customers’ inventories stayed lean at 42.3 percent, and new export orders slipped back into contraction at 48.5 percent.

Insights from the S&P Global PMI

The S&P Global US Manufacturing PMI registered 53.9 in June, down from 55.1 in May. That is a three-month low but an eleventh consecutive month above the 50 threshold. Output and new orders rose at historically elevated rates, supported by new product launches and pre-orders placed ahead of anticipated price increases.

S&P Global’s employment data was starker than ISM’s. Panel companies shed jobs at the fastest pace since May 2020 as firms worked to offset elevated energy and raw material costs. Fewer workers plus rising orders meant backlogs climbed faster than in May.

Supply chains showed renewed strain from shipping delays and port congestion, and manufacturers responded by building safety stock. Purchasing activity grew at the fastest rate in more than four years. Input cost inflation eased from May’s peak, selling price inflation cooled to a three-month low, and business confidence slipped to an eight-month low on concerns that an end to war-related inventory building could weigh on future sales.

What the Data Means

June’s reports describe a sector growing without hiring. Demand is real, but manufacturers are treating labor as the release valve for cost pressure that has built up since the Middle East conflict pushed energy and raw material prices higher. Cutting staff while orders climb pushes work into backlogs, and both surveys show backlogs building.

The price relief is the most encouraging signal in months, though costs remain well above pre-conflict levels and tariffs continue to weigh on export orders, now down for a twelfth straight month in the S&P Global survey. On the demand side, lean customer inventories should support order flow through the summer as buyers restock.

New Factory and Manufacturing Announcements

June produced another heavy slate of new factory announcements, spanning more than a dozen states and billions in committed capital. Aerospace and defense dominated, while critical minerals and semiconductor materials projects moved the U.S. closer to supply chain independence. Five projects stood out.

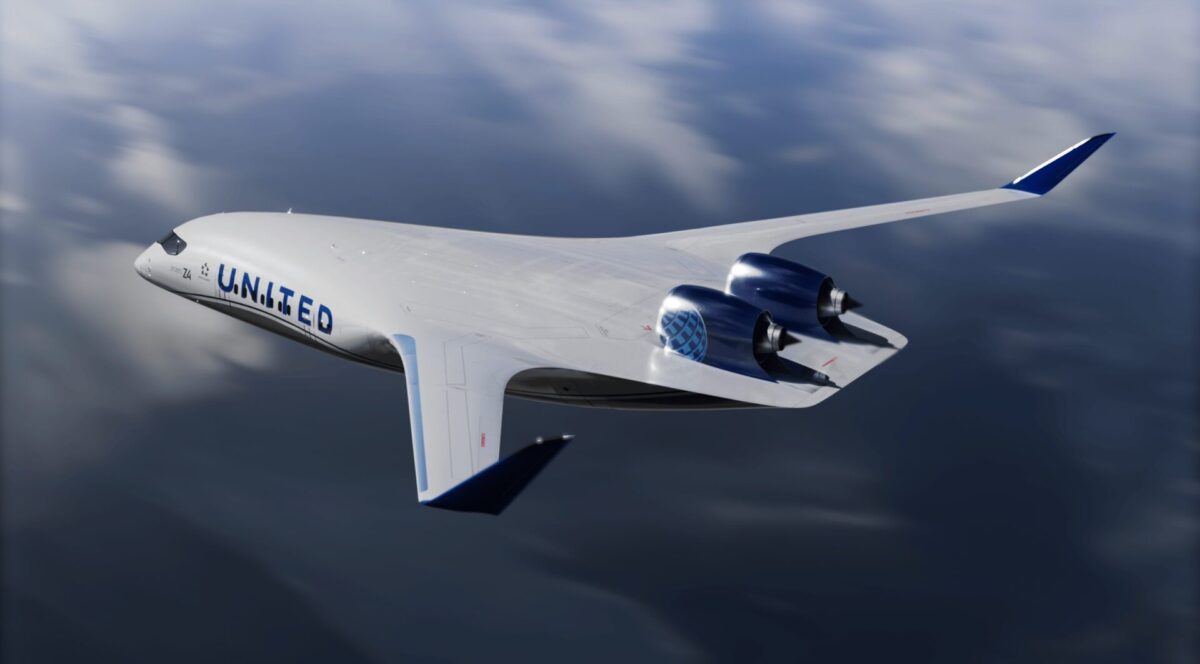

JetZero’s $4.7 Billion Aerospace Campus in North Carolina

JetZero broke ground June 15 on its first manufacturing and final assembly campus at Piedmont Triad International Airport in Greensboro, North Carolina. The 8 million-square-foot factory will rise on more than 600 acres and is expected to create more than 14,500 high-wage jobs, making the $4.7 billion project the largest economic development commitment in North Carolina history based on job creation. The startup is developing a blended wing body airliner designed to dramatically cut fuel consumption, and a greenfield assembly plant of this scale will pull an extensive supplier network toward the Piedmont Triad over the coming decade.

USA Rare Earth’s $1.2 Billion Magnet Plant in South Carolina

USA Rare Earth announced June 2 that it will build a $1.2 billion rare earth magnet and refined metals operation in Blacksburg, South Carolina. The facility targets 6,400 metric tons of neodymium-iron-boron permanent magnets and 5,000 metric tons of strip-cast metal and alloy annually, with commissioning planned for 2028 and roughly 490 high-skilled jobs.

The project carries up to $1.6 billion in CHIPS funding from the U.S. Department of Commerce. Paired with the company’s Stillwater, Oklahoma plant, the Blacksburg site pushes combined domestic capacity toward 10,000 metric tons per year, challenging China’s dominance in the magnets behind EVs, wind turbines, defense systems, and data center hardware.

Janicki Industries’ $800 Million Montana Campus

Janicki Industries announced June 2 that Great Falls, Montana will host its next manufacturing campus, an $800 million investment adding 2 million square feet of production space over the next decade. The aerospace, defense, and space supplier expects the AgriTech Park project to create 1,000 jobs within five years and more than 2,000 at completion. Construction begins in July 2026, with the first phase opening by the end of 2027.

Soulbrain’s Semiconductor Materials Plant in Texas

Texas awarded an $11.6 million Texas Semiconductor Innovation Fund grant to Soulbrain RASA TX on June 4 for a new manufacturing facility and U.S. headquarters in Taylor. The project represents more than $120 million in capital investment and will produce high-purity phosphoric acid for advanced chip fabrication, giving regional fabs like Samsung’s nearby Taylor complex a domestic source for a critical process material. Reshoring semiconductors requires more than fabs. The chemicals and materials feeding them have to localize too.

BlackVe’s Satellite Manufacturing Expansion in New Mexico

New Mexico and the City of Albuquerque announced June 19 more than $1.5 million in combined incentives to help BlackVe expand its headquarters and scale a 50,000-square-foot satellite manufacturing facility. The defense and space technology company builds multi-mission spacecraft and projects 152 high-paying jobs over the next ten years, along with more than $228 million in economic impact for the state.

Future Outlook

The second half of 2026 hinges on whether June’s price relief sticks. If de-escalation in the Middle East continues, easing energy costs should take pressure off margins and give manufacturers room to stop cutting staff. The July employment indexes deserve close attention, since a return to hiring would confirm that June’s job losses were a cost response rather than a demand signal.

The bigger question is what happens when war-related inventory building unwinds, particularly with export demand still weak under tariffs. Lean customer inventories argue against a sharp air pocket. Longer term, June’s announcements reinforced the durability of the reshoring cycle across aerospace, critical minerals, semiconductors, and defense. Those facilities will need suppliers, machinists, and materials for years to come, and the manufacturers best positioned to serve them will be the ones who protect their skilled workforce through this soft patch instead of cutting into it.